The Baltic Exchange: Bulk report - Week 28

The Baltic Exchange - Bulk report – Week 28

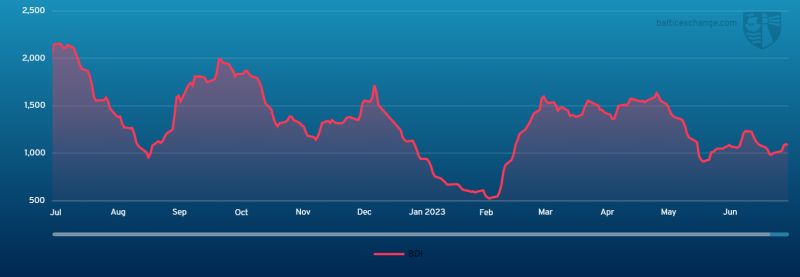

Capesize

This week began on a positive note in the Pacific market, with all three major players actively participating and securing vessels at more favourable rates. However, the momentum quickly dissipated and the market experienced a decline in rates as the week progressed, with a shift in sentiment due to a growing abundance of available vessels. The C5 market in particular experienced a decline compared to the beginning of the week. Similar downward pressure was observed in the South Atlantic market from Tubarao to China, with an increasing number of vessels in ballast, further impacting rates. By mid-week there was a stabilisation to the declining rates in the Pacific. The North Atlantic witnessed heightened activity, leading to increased volume and a scarcity of available tonnage, resulting in notable firm fixtures being concluded. As the week draws to a close, there has been continued downward pressure on rates in the Pacific. Meanwhile, in the Atlantic market, brokers expressed concerns that market conditions were shifting, possibly indicating an impending downturn. Overall, the week saw a mix of positive and negative market conditions, with fluctuations in rates and shifting sentiment. The availability of tonnage and the number of vessels in ballast were key factors influencing market trends.

Panamax

A week of positive gains for the Panamax market as the Atlantic market, both in the North and South, came to the fore once again, with EC South America absorbing tonnage worldwide, adding support to markets. The Atlantic did see better levels as the tonnage availability from the Continent and West Mediterranean tightened mid-week. From the South, a 75,000-dwt was fixed delivery EC South America end-July for a fronthaul at $14,500 plus $450,000 ballast bonus whilst an 82,000-dwt fixed delivery West Mediterranean for a trans-Atlantic run at $13,000. In Asia a mixed week with the draw from EC South America owners hardened their ideas for Indonesian business, although further north tonnage levels remained high thus rates lacked impetus despite relatively healthy amount of cargo from the NoPac and Australian regions. An 82,000-dwt fixing delivery China mid-July for a trip via Australia redelivery Singapore-Japan at $7,000. Period interest remained, an 82,000-dwt open South China fixing for a period until minimum 1 November 2024 to 15 January 2025 at $12,500.

Ultramax/Supramax

A rather mixed affair for the sector over the week. The Atlantic generally remaining in the doldrums with limited fresh enquiry or excitement. The US Gulf region bucked this trend however as sentiment remained positive, although some said it was positional. A slightly more positive feel from Asia, with better levels of enquiry from Indonesia helping rates improve slowly. Although this was tempered by a limited amount of interest from the NoPac and Australian regions. Little in the way of period action, although a 63,000-dwt open WC India was heard fixed for four to six months trading at $12,000. From the Atlantic, a 63,000-dwt was fixed for a trip from US Gulf to India at about $16,000. Elsewhere, a 53,000-dwt fixed a trip from the East Mediterranean to West Africa at $7,000. From Asia, a 56,000-dwt fixed delivery Singapore for a trip via Indonesia redelivery China at $10,000. Whilst a 56,000-dwt was heard fixed from CJK via Australia redelivery Singapore-Japan at about $6,500.

Handysize

The systematic erosion of levels across the sector continued with the ongoing lack of enquiry ensuing in a growing number of open vessels. On the Continent, a 34,000-dwt was fixed from North France to Morocco with an intended cargo of grains in the $4,000s. A 34,000-dwt fixed basis delivery Canakkale via Novorossiysk to Algeria at $10,000, whilst at the end of the week a 32,000-dwt was fixed for a similar trip at $7,000. In Asia, a 39,000-dwt opening in Taiwan was fixed via Indonesia to Vietnam with an intended cargo of coal in the mid-$7,000s. A 40,000-dwt opening in Mikawa was fixed for a trip to the Mediterranean with an intended cargo of steels in the high $7,000s and a 35,000-dwt opening in South China was fixed basis delivery in Indonesia to the Mediterranean in the low $6,000s. A 35,000-dwt opening in Southeast Asia was fixed for eight to 10 months with worldwide redelivery in the $8,000s.

Similar News